Pratt & Whitney Archives - Leeham News and Analysis

GE Aerospace has announced that CFM International LEAP engines currently rolling off production lines have achieved durability levels matching the industry-standard benchmark set by the CFM56, fulfilling a commercial promise that dates back to the engine's competitive launch in 2010. The LEAP family — comprising the LEAP-1A on the Airbus A320neo, the LEAP-1B exclusively powering the Boeing 737 MAX, and the LEAP-1C on the COMAC C919 — entered service beginning in 2016 and 2017 alongside Pratt & Whitney's Geared Turbofan. Both engine programs fell materially short of their guaranteed on-wing time in the years following entry into service, meaning components degraded and required removal far earlier than operators had been promised. GE's announcement represents a significant engineering milestone, achieved through an extended testing and refinement regimen that the company has documented publicly, including innovations such as foam wash procedures aimed at preserving hot-section components and reducing the accelerated wear associated with ingested particulates and environmental contaminants.

The durability shortfalls of both the LEAP and GTF programs have had serious operational and financial consequences for airlines and lessors operating narrowbody fleets over the past several years. While Pratt & Whitney's situation became the more acute crisis — with a powder metal contamination issue discovered in GTF high-pressure compressor and turbine discs grounding upward of 700 A320neo-family aircraft, dozens of Airbus A220s, and a number of Embraer E195-E2s simultaneously — the LEAP program generated its own pattern of premature engine removals and unscheduled shop visits. For operators, the practical effect was identical regardless of engine type: the double-digit fuel burn savings that both programs advertised were substantially eroded by higher-than-projected maintenance costs, increased shop visit frequency, and associated aircraft-on-ground disruptions. Airlines that built business cases around LEAP and GTF economics found their cost-per-available-seat-mile assumptions compromised at precisely the moment jet fuel prices were climbing sharply, with IATA tracking jet fuel near $197 per barrel as of late March 2026.

For professional pilots and flight operations departments, the LEAP durability news carries direct relevance to dispatch reliability, MEL exposure, and fleet planning assumptions. Operators of 737 MAX fleets — which rely exclusively on the LEAP-1B with no alternative powerplant option — have been particularly exposed to maintenance-driven schedule disruptions, since there is no engine substitution flexibility as exists on the A320neo family. If GE's claim holds in revenue service, the practical result should be longer average time on wing, fewer unscheduled removals, and improved aircraft availability for operators conducting high-cycle short-haul operations where engine exposure accumulates rapidly. Corporate and charter operators flying the MAX variant in Part 135 or 91K environments similarly stand to benefit from reduced AOG risk and more predictable heavy maintenance intervals when planning long-term lease structures and charter availability commitments.

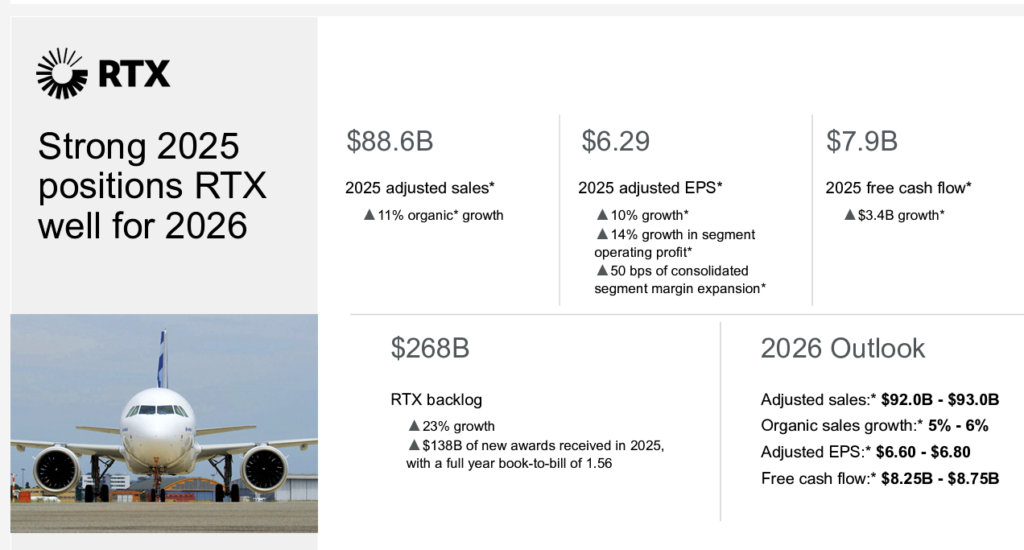

The broader context framing this development is an industry under sustained production and supply chain stress. As Leeham's analysis of commercial engine OEM economics makes clear, powerplant manufacturers across all tiers face structural capacity constraints that cannot be resolved quickly, and engine shortfall is the common limiting factor behind both Airbus and Boeing production-rate ambitions. RTX closed 2025 with a record $268 billion backlog and continued progress on the GTF powder metal remediation, signaling that the industry's two dominant narrowbody engine suppliers are both in active recovery mode. GE's durability milestone, if validated across the broader in-service LEAP population, would represent a stabilization of one side of that equation. Meanwhile, longer-horizon questions about next-generation propulsion — including CFM's RISE open-fan program and the engine architecture debates surrounding blended wing body concepts like JetZero's Z4 — underscore that the commercial aviation industry is simultaneously managing near-term reliability crises while committing billions to technology transitions that will define the next 30 years of narrowbody and midsize aircraft operations.

Read original article

Read original article