How Pratt & Whitney's Game-Changing GTF Engine Created Problems Airlines Weren't Prepared For

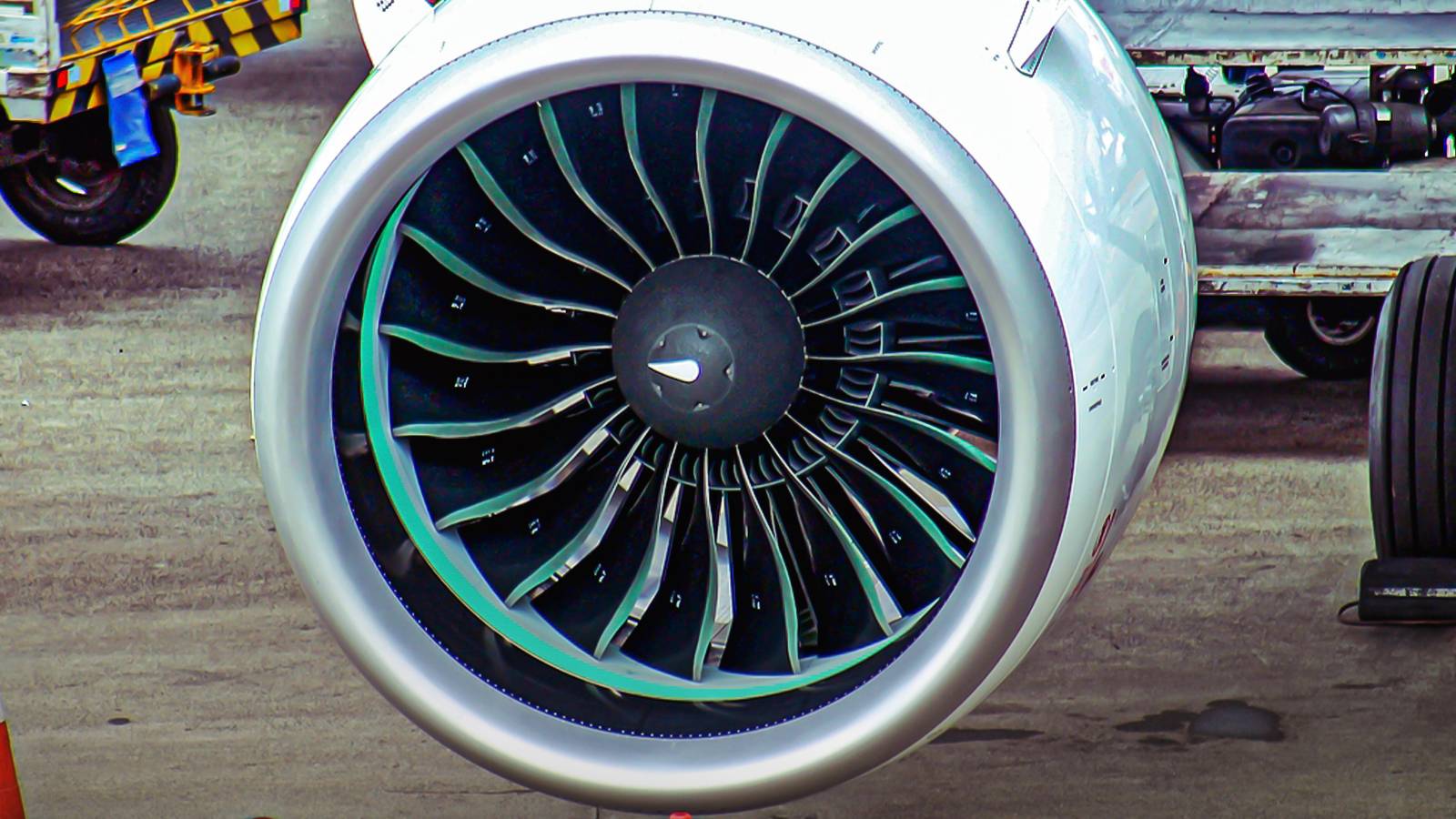

Pratt & Whitney's Geared Turbofan engine arrived in commercial service as a genuine engineering breakthrough, resolving a decades-old aerodynamic compromise that had constrained turbofan efficiency since the high-bypass era began. By inserting a precision reduction gearbox between the low-pressure turbine and the front fan, the GTF allowed each component to spin at its aerodynamically optimal speed — the fan at roughly 3,000 RPM and the turbine approaching 10,000 RPM — a configuration impossible in conventional direct-drive architecture. The result was an engine family, anchored by the PW1100G, that delivered fuel burn reductions of up to 20 percent and measurable gains in noise and emissions performance across the Airbus A320neo and A220 families. The gearbox itself, less than a foot in diameter yet capable of transmitting more than 30,000 horsepower, stood as one of the more remarkable feats of precision engineering in modern propulsion design. Airlines signed onto GTF-powered fleets in large numbers, and within a few years the platform had collectively saved more than one billion gallons of fuel globally.

The crisis that followed was not a failure of the gearbox concept itself but rather a manufacturing contamination defect embedded in powder-metal components used in critical engine sections. Engines built between 2015 and 2021 contained microscopic cracks introduced during the powder-metal production process, and those cracks could propagate under normal operational stress, creating risk of serious in-service failures. Once regulators responded with mandatory accelerated inspection intervals, the global maintenance system was overwhelmed almost immediately. Shop turnaround times that had averaged 60 to 90 days ballooned to 250 to 300 days at the crisis peak, and at maximum severity approximately 835 aircraft — nearly 40 percent of the worldwide GTF-powered A320neo fleet — were grounded simultaneously. Spare engine availability collapsed, with some GTF units commanding lease rates around $200,000 per month, and operators began cannibalizing relatively young aircraft solely to extract serviceable engines and parts.

For airline operations and fleet planners, the GTF crisis delivered a hard lesson about concentration risk in next-generation powerplant programs. Airlines that had standardized heavily on GTF-powered narrowbodies found themselves unable to hedge against the grounding wave because the defect was systemic across the production run rather than isolated to specific operators or maintenance practices. The MRO infrastructure — capacity, tooling, trained technicians — had been built around a normal maintenance cadence and could not rapidly scale to absorb hundreds of simultaneous unscheduled shop visits. Schedule reliability collapsed at affected carriers, and the secondary market consequences, including asset value distortions and lessor disputes, continued to ripple through the aviation finance sector long after the immediate inspection crisis stabilized. The episode underscored that even a technically successful engine program carries systemic fleet-level exposure when a single manufacturer and powerplant variant dominates a major aircraft category.

The broader implications for business aviation and Part 91 operators are somewhat indirect but still instructive. The GTF platform does not power typical business jets, but the crisis accelerated scrutiny of single-source propulsion dependencies across all segments of commercial and corporate aviation. MRO capacity constraints that originated in the GTF crisis contributed to broader shop workload backlogs affecting the entire engine overhaul ecosystem, with labor, tooling, and parts resources diverted toward the most urgent regulatory mandates. Pratt & Whitney's response — billions in manufacturing expansion and the introduction of the FAA-certified GTF Advantage variant with redesigned components — represents an attempt to restore confidence in the platform, but the Advantage's full benefit will take years to propagate through fleets still carrying engines from the affected production window. Operators and flight departments evaluating aircraft with next-generation powerplants are now applying greater scrutiny to spare engine availability, MRO contract terms, and the systemic exposure associated with fleet-wide powerplant commonality.

The GTF episode ultimately represents a cautionary case study in the gap between propulsion technology ambition and supply-chain execution readiness. The geared turbofan architecture itself remains sound and has delivered on its core efficiency promises, but the industry-wide dependence on a single manufacturer's production ramp — without adequate contingency planning for a systemic defect — created a fragility that no operator had fully modeled. As the aviation industry continues pursuing next-generation propulsion across both commercial narrowbodies and emerging hybrid-electric platforms, the GTF crisis will serve as a reference point for regulators, OEMs, lessors, and operators alike when assessing how quickly a technology transition can generate consequences that outpace the maintenance and logistics infrastructure built to support it.

.jpg?q=50&fit=crop&w=32&h=32&dpr=1.5)