Comac Archives - Leeham News and Analysis

Airbus faces a conspicuous absence in one of the world's most consequential aviation markets: despite operating an A320neo family final assembly line in Tianjin, an A330 finishing line, and an extensive network of Chinese suppliers, the company has never secured a single A220 order from China. That gap persists even though Chinese manufacturing has been embedded in the A220 program since its Bombardier C Series days, with Shenyang producing fuselage sections that are shipped to Mirabel, Quebec, for final assembly. Airbus executives, speaking at a June 24, 2026, media briefing at Airbus Canada's Mirabel headquarters, identified a specific political wound as the root cause: when Bombardier sought buyers for the struggling C Series program around 2017, Chinese entities were active bidders, and Beijing's exclusion from that deal in favor of Airbus left lasting resentment. Christian Kley, head of single-aisle market development, acknowledged bluntly that "they have long memories."

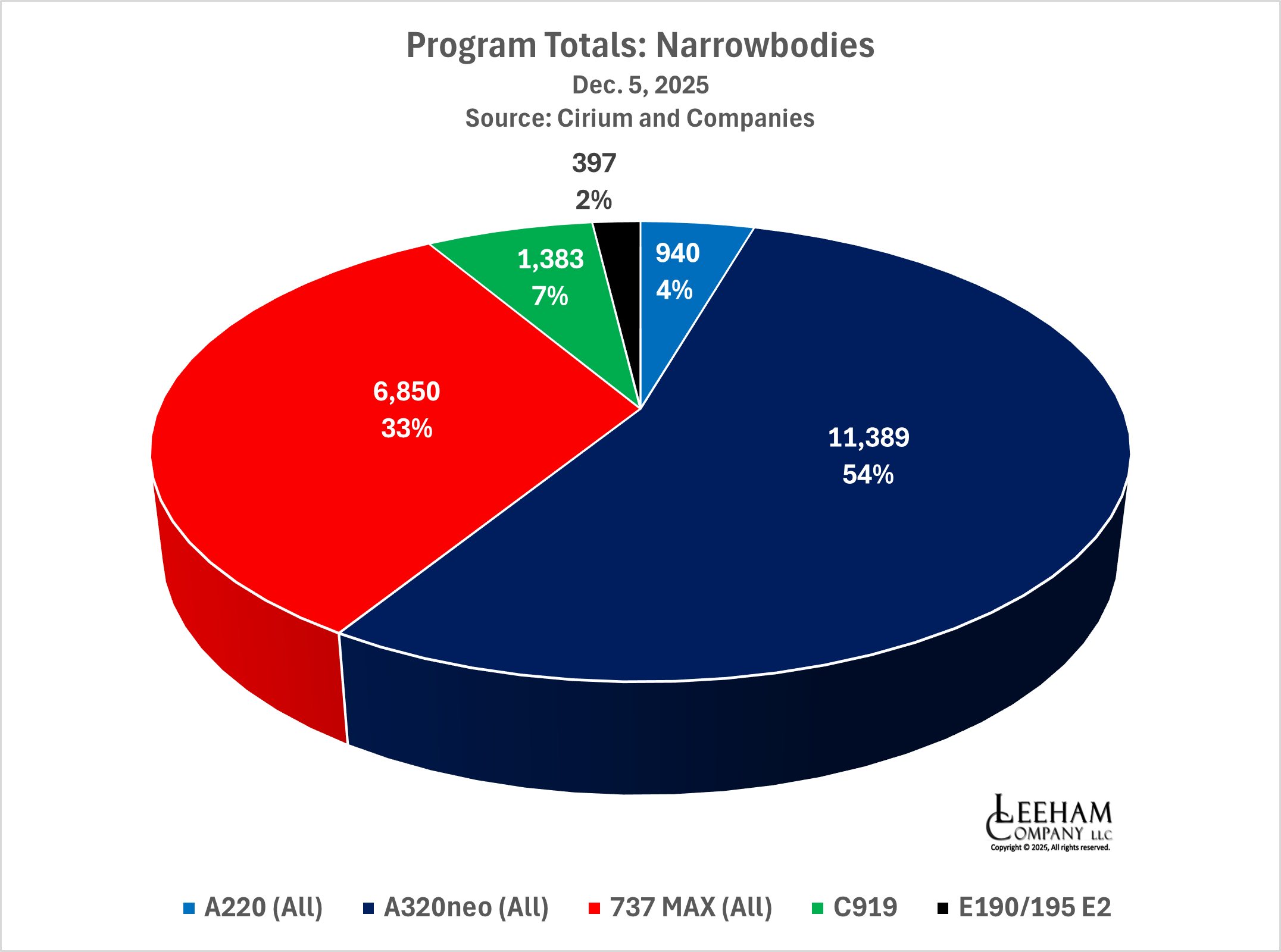

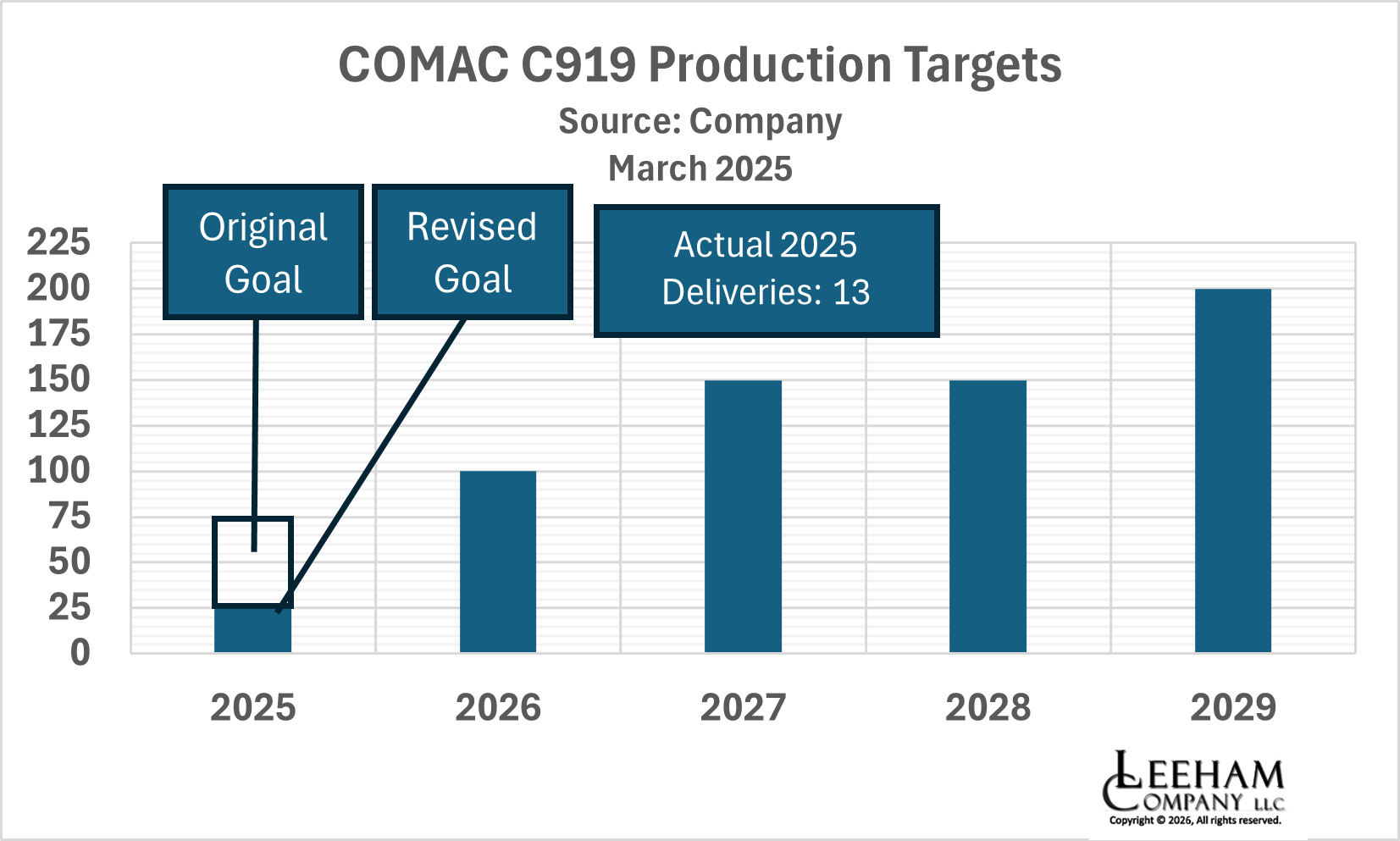

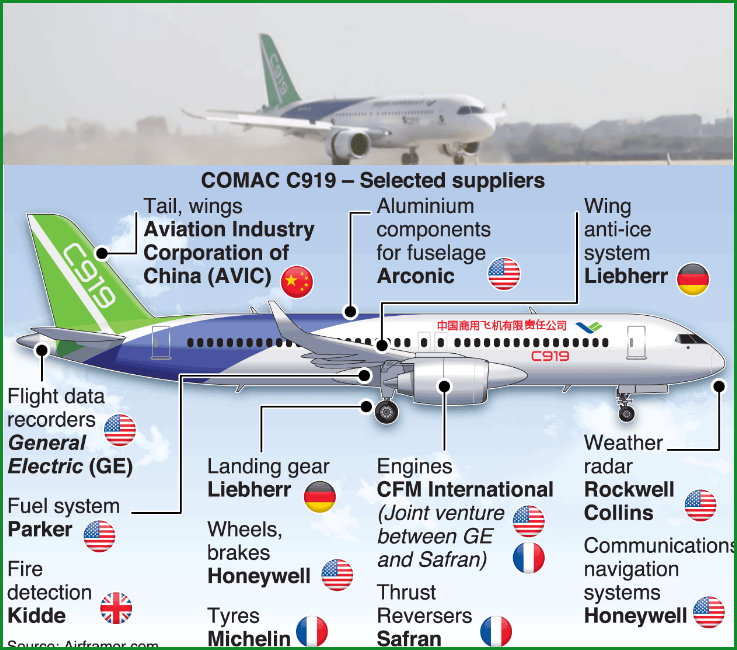

COMAC's own trajectory provides critical context for understanding why Chinese aviation politics matter so acutely to Western airframers. China's state-owned commercial aerospace manufacturer targeted 75 C919 deliveries in 2025 but was forced to revise that figure down to 25, ultimately delivering approximately 13 aircraft — matching its 2024 output and underscoring the severity of disruption caused by Western sanctions tied to China's support of Russia in the Ukraine conflict. The C919, designed to compete with the Airbus A320neo and Boeing 737-8, carries over 1,000 orders, though the overwhelming majority reflect government mandates to Chinese carriers and lessors rather than open-market competition. Despite those structural limitations, Leeham's analysis places the C919 at roughly 7% of the 100–240-seat single-aisle backlog — a captive but growing share that cannot be ignored as China trends toward becoming the world's single largest aviation market.

The broader single-aisle competitive picture reinforces how much is at stake in China. Airbus holds approximately 54% of the A320neo family's program orders versus Boeing's 33% for the MAX family; adding the A220 pushes Airbus's single-aisle share to 58%. Boeing's erosion from a position of rough parity stems from its 2011 decision to derivative-extend the 737 rather than launch a clean-sheet replacement, compounded catastrophically by the 737 MAX crises beginning in March 2019. For Boeing, China access represents a potential lifeline, with reports from August 2025 suggesting the two sides were approaching a substantial order agreement. For Airbus, closing the A220 gap in China could meaningfully reinforce its already dominant single-aisle position and provide a counterweight to any Boeing-Beijing deal.

For professional flight operators and aviation business planners, these dynamics carry concrete fleet implications. Airlines and lessors evaluating narrowbody capacity through the 2030s must account for the possibility that COMAC's C919 — despite its current production limitations and near-total dependence on government-directed orders — will mature into a credible regional competitor as China internalizes more of its supply chain and works around Western component restrictions. The C909 regional jet, despite being a derivative of 1960s Douglas technology powered by GE CF-34 engines also used on the CRJ and Embraer E1, similarly reflects a state industrial strategy prioritizing long-term capability building over near-term commercial efficiency. Operators flying into or out of China, or evaluating Chinese-manufactured components in their aircraft, should monitor how sanctions enforcement and trade policy continue to affect COMAC's production ramp and component access, as those constraints directly influence delivery reliability and maintenance support pipelines.

The interplay of geopolitics, industrial policy, and commercial aviation strategy visible in the China market represents a structural shift in how aircraft orders are won and allocated globally. Airbus's attempt to rehabilitate its standing with Beijing over the A220 — a decade after a political slight over a Canadian transaction — illustrates how long procurement decisions can be shaped by factors entirely outside an aircraft's technical or economic merits. For operators and fleet planners in the business jet and commercial sectors alike, the lesson is that supply chain geography, sanctions exposure, and government relationships are now first-order variables in assessing aircraft availability, parts support continuity, and long-term fleet residual values in ways that would have seemed peripheral just a decade ago.

Read original article

Read original article