Updated with CEO comments: Air Asia orders for 150 A220s, giving program a big boost; launches high density version - Leeham News and Analysis

AirAsia's firm order for 150 Airbus A220-300s, announced May 6, 2026, marks the largest single-transaction purchase in the A220 program's history and pushes total A220 firm orders past the 1,000-unit threshold. The deal, valued at approximately USD 19 billion at list prices, was signed at Airbus's Mirabel, Quebec final assembly line in the presence of Canadian Prime Minister Mark Carney and Quebec Premier Christine Frechette — a geopolitically loaded backdrop reflecting the order's significance to Canada's aerospace industrial base. Options for up to 150 additional aircraft bring the potential total to 300 A220 family jets for the AirAsia group. Deliveries are expected to begin in early 2028, with the aircraft serving Southeast Asian, Central Asian, and broader Asia-Pacific routes. As of late March 2026, 501 A220s had been delivered to 25 operators worldwide, meaning AirAsia's order alone represents a commitment roughly equal to 30 percent of the total fleet currently in service.

The strategic rationale articulated by Capital A CEO Tony Fernandes centers on right-sizing capacity against AirAsia's route network structure, a consideration directly relevant to fleet planners and operators managing mixed narrowbody fleets. Fernandes noted that roughly 60 percent of AirAsia's routes serve secondary and tertiary cities that were previously unserved, and that even on dense corridors like Kuala Lumpur–Singapore, half-hourly frequency schedules cannot consistently fill 244-seat A321neos. A 160-seat A220-300 operating those same frequencies improves unit economics — Fernandes estimated a two-to-three point margin improvement — without the capacity risk of deploying a larger narrowbody. The A220-300's published range of up to 3,600 nautical miles also significantly exceeds the A320ceo it replaces; Fernandes specifically highlighted the jump from roughly four-hour A320ceo range to seven hours on the A220-300, a parameter that opens new point-to-point routes across the broader Asian geography without requiring widebody equipment or fuel stops.

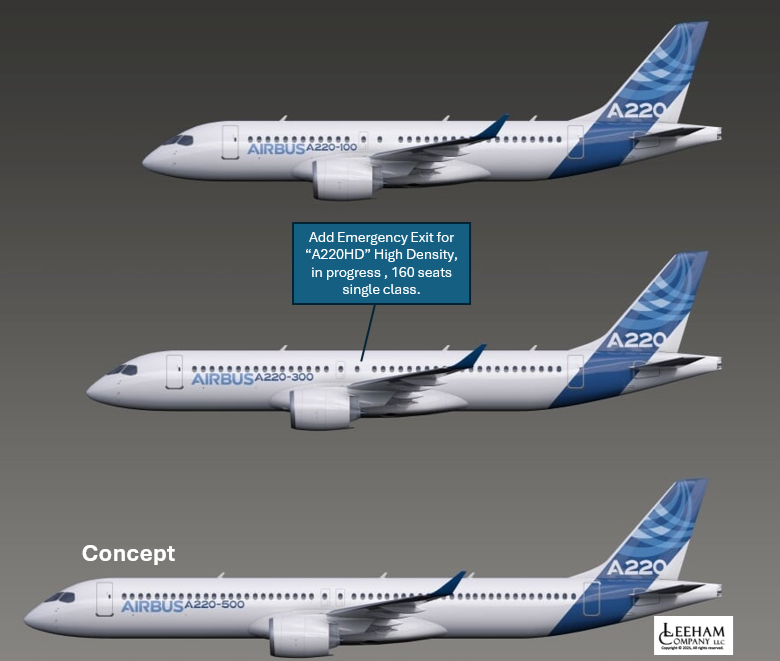

AirAsia's role as launch customer for the 160-seat high-density A220-300 configuration adds a product development dimension to the order. The current standard A220-300 cabin accommodates 100 to 150 passengers depending on layout; achieving 160 seats requires adding one overwing emergency exit per side to satisfy certification requirements at that occupant load. This configuration directly targets the gap between a full-sized narrowbody and a traditional regional jet, positioning the A220 as a competitive alternative to the A320ceo on thinner routes where operators have historically accepted the inefficiency of larger equipment or reduced frequencies. For Part 121 carriers evaluating fleet renewal, the high-density variant signals that the A220-300's practical seating ceiling is moving upward, narrowing the capacity differential with the A319neo and lower-density A320neo configurations.

The order's production implications are substantial for Airbus and for the crews and operators who will eventually fly these aircraft. Airbus has targeted an A220 production rate of 14 aircraft per month but has acknowledged that the backlog, prior to this transaction, was insufficient to sustain that rate with confidence. The revised internal timeline now pushes rate-13 to the end of 2028. AirAsia's 150-unit firm order provides the backlog depth needed to justify the Mirabel line's ongoing investment and workforce stability, a factor the Canadian government's high-level participation in the announcement made explicit. For pilots tracking type rating supply and demand, a program accelerating toward 14 per month with a major new LCC operator absorbing aircraft through the early 2030s signals growing demand for PW1500G-type qualified crews across Southeast Asia, a market that has been chronically pilot-constrained since the post-pandemic traffic recovery.

Fernandes's public advocacy for an A220-500 stretch — configured at approximately 180 seats — frames the broader competitive significance of this order for Airbus's narrowbody product line. An A220-500 at that capacity would slot directly into the replacement tier for aging A320ceo and early A321ceo fleets operated by LCCs that cannot economically justify the A321neo's higher seat count on thinner routes. Airbus has been weighing the stretch program against engineering and certification cost; a committed launch customer of AirAsia's scale materially strengthens the business case. For operators and lessors evaluating narrowbody fleet strategy in the 150-to-200 seat segment, the A220-500's eventual launch — or continued deferral — will have significant implications for residual value trajectories on current A319neo and A320neo equipment, as well as for the competitive positioning of Boeing's 737 MAX 8 in markets where the MAX has no direct A220-family competitor.

Read original article

Read original article